This article is free for you and free from outside influence. To keep things this way, we finance it through advertising, ad-free subscriptions, and shopping links. If you purchase using a shopping link, we may earn a commission. Learn more

Flying High

Aerospace Industry’s Demand for 3D Printing Valued at $1.6 Billion

New research by VoxelMatters reveals the aerospace industry invested heavily in 3D printing tech and services in 2023 with demand set to increase to $20.5 billion by 2033.

Advertisement

According to new market research from VoxelMatters, the aerospace industry bought more than $1.5 billion worth of 3D printers, printing materials, related hardware, parts and services in 2023. What specifically they’re 3D printing with this technology is seldom revealed, but aerospace is adopting metal and polymer 3D printing at record levels, according to VoxelMatters.

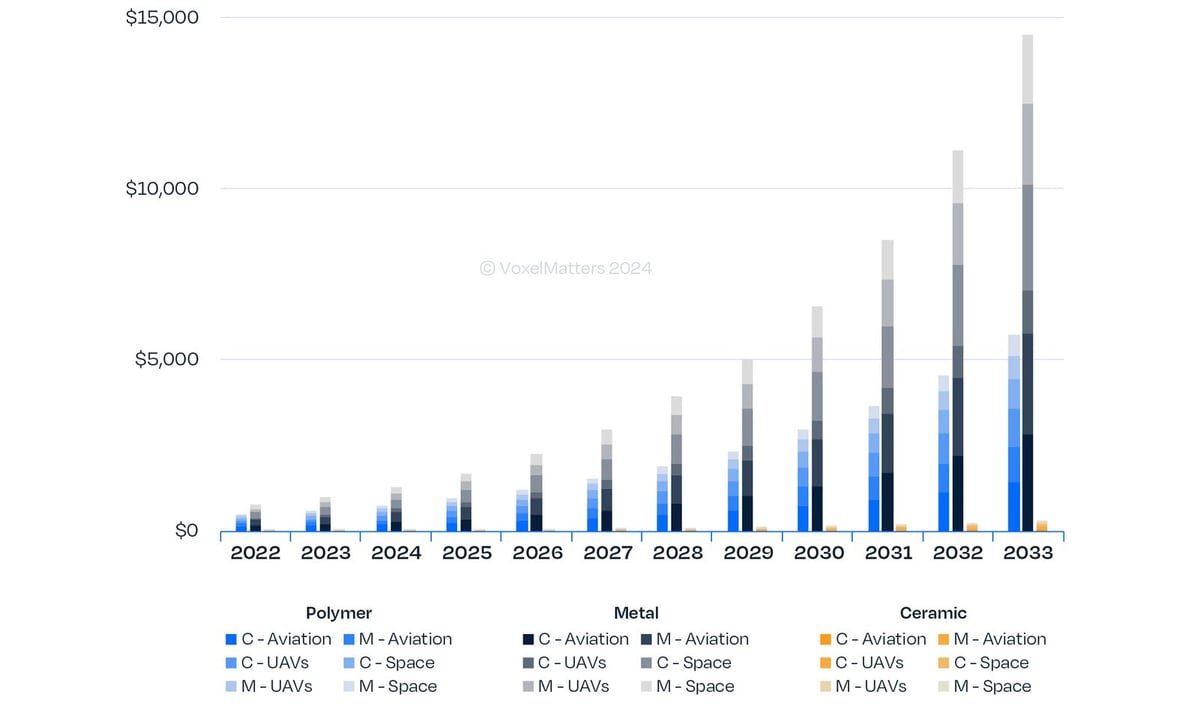

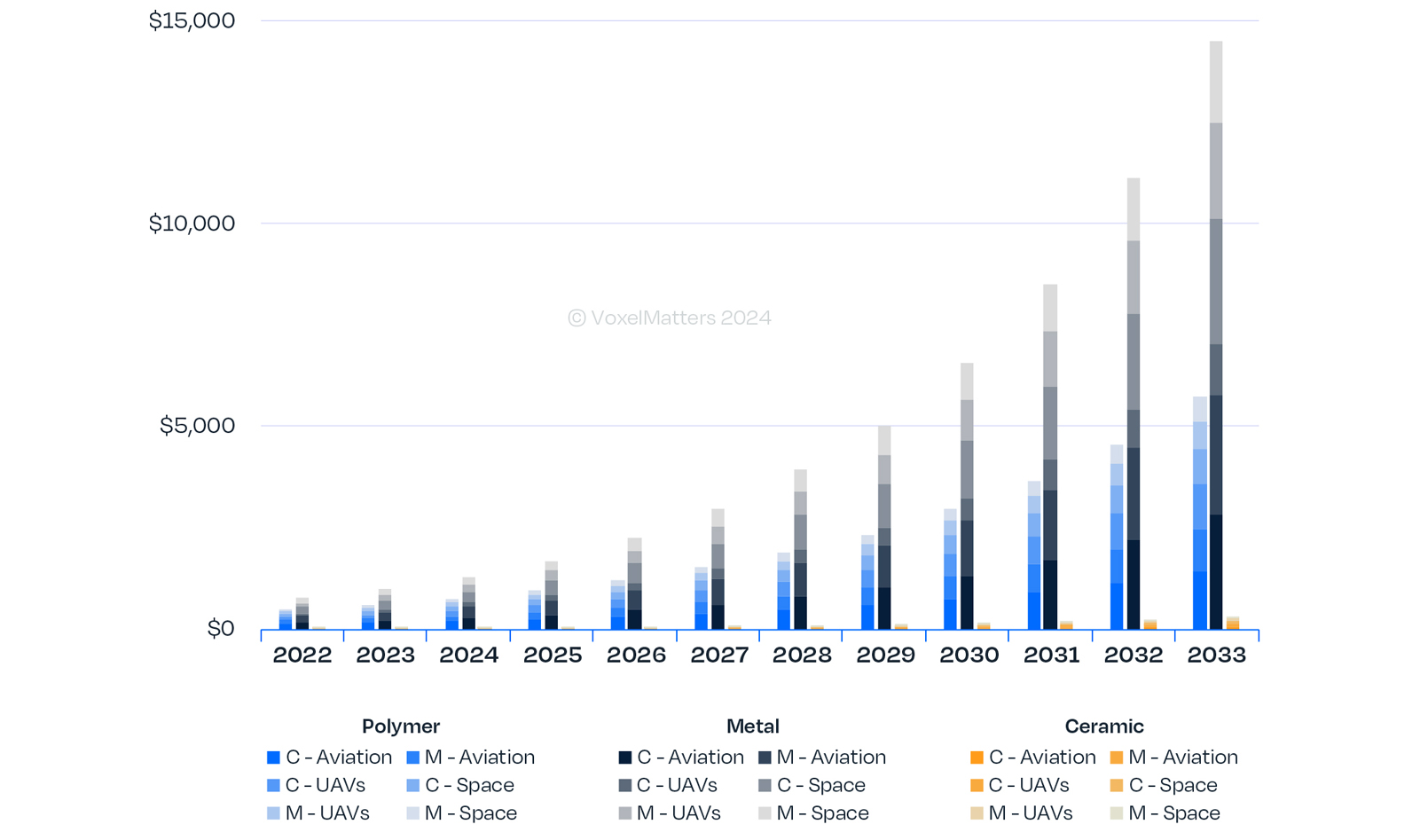

In fact, this market is expected to expand into a $20.5 billion opportunity over the next ten years, with a compound annual growth rate (CAGR) of 29%.

“The aerospace sector – driven in part (but not only) by growing demand for defense applications – is currently one of the most important users of additive manufacturing (AM) technology,” says Davide Sher, co-founder and CEO at VoxelMatters. “This is also probably one of the most mature segments for AM adoption, with applications including prototypes, tools but also, increasingly, final parts already driving industry revenues and revenue growth.”

This new market study offers an analysis and forecast of 3D printed metal, polymer, and technical ceramics in aerospace parts manufacturing, focusing on the hardware, materials, and services segments of the additive manufacturing market. Researchers looked at data on AM part production by industry end-user companies in aerospace manufacturing, including Airbus, Boeing, Lufthansa Technik, Rolls Royce, SpaceX, Northrop Grumman, and Ursa Major, as well as data from 3D printer maker, services, and material providers.

One example of 3D printing in aerospace is the 3D printed fuel nozzles in the GE Aerospace CFM LEAP engines, produced jointly by GE and its long-time partner, Snecma of France. GE just announced that Avolon, a global aviation finance company, ordered 150 LEAP-1A engines to power 75 A320 aircraft. GE also has 3D printed parts in its GEnx and GE9X engines with new commitments recently secured from EVA Air to power four 787s and Qatar Airways for 40 GE9X engines to power 20 777s.

Advertisement

Advertisement

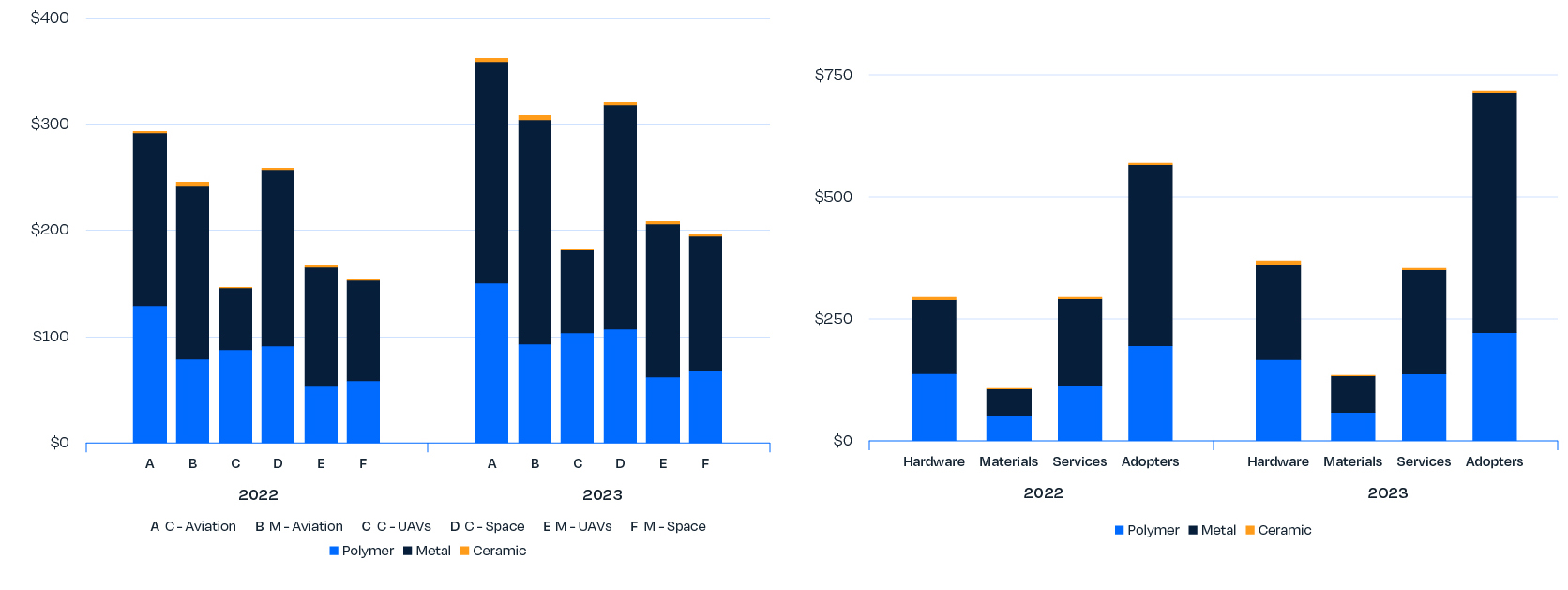

Overall, the aerospace AM market was largely driven by “adopters”, a term VoxelMatters uses to describe aerospace industry end-users that include OEMs, tier-one and tier-two suppliers, and some contract manufacturers that specialize in aerospace. Other than adopters, the market is made up of AM service providers and suppliers, and hardware and material suppliers.

Adopters made up 45.5% of total revenue in 2023 at $718 million, while hardware sales were 23.5% ($370 million) of total revenue, and services accounted for 22.5% ($355 million). Material sales, the smallest subsegment, contributed 8.5% with revenues of $134 million.

Civil & Military Aviation Nearly Equal in 3D Printing Use

In 2023, civil aviation — companies such as Boeing and Airbus — was the largest contributor to the market, accounting for 22.9% of the share, while military aviation was a close second at 20.3%. The rest of the market pie is divided by civil space (19.5%) companies such as SpaceX, military space (13.2%), military unmanned aerial vehicles (UAVs) or drones accounted for 12.5% of revenues, and civil UAV (11.6%) companies, such as Krato.

Metal 3D printing dominated in the aerospace market for 3D printing. It accounts for 62% of total market revenues with “adopters” generating half of the metal revenues, amounting to an estimated total of $492 million. Sales of metal materials, typically powders, accounted for 7.8% of metal revenue, increasing by 35.9% over 2022 estimates. Metal materials accounted for just over half of all material sales to the aerospace market, rising to $76 million.

Similarly, metal 3D printers accounted for the largest portion of hardware sales to this market, contributing 53.1% of total hardware revenue, which grew by 29% to $196 million (12.4% of the total market). In the material subsegment, metal materials accounted for 56.7% of revenues, rising by 35.9% to $76 million (4.8% of the market). Metal AM services led the services subsegment, comprising 60.2% of total revenue and growing by 20.7% to $214 million (13.5% of the market).

“We were particularly impressed by the dominance of metal AM products, including hardware, materials and parts, in terms of generated revenues,” says Sher. “Right now powders and powder based processes are certainly the ones dominating the market both in terms of parts produced and generated revenues.”

Polymer 3D printing has had a significant impact in civil UAVs, contributing 56.5% of polymer revenues. Although technical ceramic AM remains niche, it has seen substantial growth due to civil space applications because of the material’s suitability to extreme environments.

Advertisement

Advertisement

Aerospace AM in 2033

Aerospace AM is projected to exceed $20 billion in sales value by 2033 with hardware revenue projected to reach $3.9 billion.

Adopters are expected to account for 51% of the market, while the hardware share is anticipated to decline to 19%, confirming the sector’s maturity relative to other technology-driven areas of AM. This subsegment is forecasted to reach $10.5 billion, with metal adopters generating 77.5% of the value. Hardware revenue is projected to reach $3.9 billion, with metal hardware at 53.2%, polymer at 43.4%, and technical ceramics at 3.5%. Material revenue is expected to reach $1.7 billion, with metals leading at 70.3%. Services are projected to contribute $4.5 billion, predominantly from metal services, which will account for 69.8%.

____________________

VoxelMatters’ Aerospace AM 2024 full report is available for around $4,500 at VoxelMatters Research.